A Guide to New Home Builder Incentives in North Texas

- scott shipp

- Feb 15

- 13 min read

Building a new home here in North Texas is a huge milestone, and if you play your cards right, new home builder incentives can make the deal even sweeter. These aren't just marketing gimmicks; they are serious financial tools that builders use to keep projects moving in competitive markets like Granbury and Weatherford. We're talking everything from mortgage rate buy-downs to generous design center credits that can save you thousands.

Decoding Builder Incentives in the Texas Market

When you're looking at new construction in places like Glen Rose or Stephenville and see an ad for thousands of dollars in savings, a little skepticism is healthy. But let me set your mind at ease: these incentives are a standard, valuable part of the home-building business, not a red flag. Builders use them to hit specific business goals, and that creates real opportunities for you.

Understanding the "why" behind an offer is the key. A builder needs to maintain a certain sales pace to manage their cash flow and keep construction schedules on track. Incentives help them do that without dropping the sticker price of the homes, which is a good thing because it protects the property values for everyone who buys in that community.

Why Incentives Are So Common Today

The market for new homes is always changing, and incentives have become much more common as builders compete for your business. Fluctuating interest rates or the need to sell the last few homes in a community often push builders to get more creative with their deals.

This is great news for homebuyers across North Texas. In fact, according to the National Association of Home Builders (NAHB), a significant majority of builders now offer sales incentives to attract buyers. In competitive markets, it's not uncommon to see builders offer perks to maintain sales momentum.

Key Takeaway: Don't think of a builder incentive as just a simple discount. It's a strategic negotiation tool. The real goal isn't just to grab the first offer you see, but to figure out its true value and how it fits into your long-term financial picture for your new Texas home.

Shifting Your Mindset for Success

It's easy to get caught up asking, "How much can I save?" But a much better question is, "Which incentive gives my family the most value over the long haul?" For one family building on rural land near Weatherford, locking in a lower interest rate for the life of the loan is the biggest win. For another couple planning their retirement home in Granbury, getting a high-end kitchen appliance package without dipping into savings is the game-changer.

When you understand the different kinds of incentives and how they connect to smart spending, you can be sure you’re getting the most for your money. To learn more about making every dollar count, check out our North Texas homeowner's guide to value engineering. Our goal is to pull back the curtain on these offers so you can make decisions you feel great about.

What Kind of Incentives Are We Talking About?

Builder incentives aren't all cut from the same cloth. A deal that saves one family a ton of money in Stephenville might not be the right fit for another buyer over in Cleburne. Getting a handle on these different types of deals helps you look past the big, flashy numbers and see which incentive actually puts the most money back in your pocket.

Let's break down the most common incentives you'll run into here in North Texas so you know exactly what you’re looking at.

Mortgage Rate Buy-Downs

With interest rates being what they are, a rate buy-down is easily one of the most powerful tools in the shed. Here’s how it works: the builder pays a lump sum to their lender, which in turn "buys down" your mortgage rate for the first few years. This can dramatically lower your monthly payment right when you need it most.

A common example is a 2-1 buy-down. Let's say you have a $450,000 loan at a 6.5% interest rate. The buy-down could drop your rate to 4.5% for the first year and 5.5% for the second, before it settles back at 6.5% for the rest of the loan. That's a huge monthly saving that frees up cash for furniture, landscaping, or just getting comfortable in your new Weatherford home without feeling stretched thin.

Closing Cost Assistance

Scraping together cash for the down payment and closing costs is a huge hurdle for many families. This incentive tackles that head-on. The builder agrees to cover a chunk—or sometimes all—of those upfront fees.

Closing costs in North Texas can range from 2% to 5% of the loan amount and typically include:

Loan origination fees

Appraisal and inspection costs

Title insurance

Prepaid property taxes and homeowners insurance

A builder might offer something like $10,000 toward closing costs. On a $500,000 home, that’s a massive relief. It means you don't have to drain your savings just to get the keys.

My Two Cents: Always ask for an itemized list of what the closing cost credit covers. Some offers are pretty rigid. Getting the details upfront ensures there are no last-minute surprises when you're signing papers for your new place in Granbury.

Design Center Credits and Upgrades

For most of our clients, this is the fun part—picking out all the finishes that make a house your home. A design credit is basically a shopping spree on the builder. You get a set dollar amount to spend on upgrades like premium countertops, gorgeous flooring, or that high-end appliance package you’ve been eyeing.

For example, a $15,000 design credit could allow you to swap standard laminate for stunning quartz in the kitchen and bathrooms or put it toward beautiful engineered hardwoods in the main living areas. It's a way to get those personalized, high-quality touches you want without having to pay more out-of-pocket.

Lot Premium Waivers and Financing Concessions

In new communities around Glen Rose and Tolar, the best lots—the ones on a quiet cul-de-sac, with a great view, or backing up to a green space—often come with a "lot premium." This extra charge can add anywhere from $5,000 to over $50,000 to the price tag. A fantastic incentive is when a builder simply waives that fee, letting you snag a prime piece of land for the standard price.

Finally, some concessions are tied to using the builder's preferred lender. You should always compare rates, but these can be great deals. The builder might offer to pay for your appraisal or cover other lender fees if you finance with their partner. To see how these different incentives might impact your bottom line, a tool like our North Texas custom home construction cost calculator can give you a clearer picture of the total cost.

How to Negotiate the Best Deal for Your New Build

Landing the best incentive package for your new home in North Texas isn't about hardball tactics. It’s a conversation, not a confrontation. The real key is understanding the builder's motivations. If you can help them hit one of their targets, you create natural leverage to ask for something you value in return.

Timing Your Conversation is Everything

In real estate, timing can make all the difference. Builders often have quarterly or year-end sales goals breathing down their necks. If you're ready to sign a contract near the end of a fiscal period, they might be much more willing to sweeten the pot to hit their numbers. This is a huge opportunity for buyers in places like Weatherford or Granbury.

Another golden moment is during the final phase of a community. Builders hate carrying the costs of just a few unsold lots or spec homes. They’re usually eager to close out the development and move on, which can open the door for more generous new home builder incentives.

Do Your Homework and Create Your Leverage

Walking into a sales office armed with knowledge is your single greatest asset. Before you even think about talking numbers, do your research on comparable new builds in the area. What are other builders in Glen Rose or Stephenville offering for similar homes?

You'll want to dig into a few key factors:

Base Prices: Are the prices in the same ballpark for similar square footage and features?

Standard Features: Does one builder include granite countertops as standard while another charges you for an upgrade?

Current Incentives: Is a competitor openly advertising $15,000 in closing costs or a major rate buy-down?

When you have this information, you can frame your requests based on what the local market is doing. Instead of just asking for a discount, you can say, "We love this floor plan, but we noticed a similar builder nearby is including a full appliance package. Is that something you can match to earn our business?" This instantly shows you're a serious, informed buyer. To get fully prepared, it's a great idea to review the top 10 questions to ask custom home builders in North Texas.

The Art of the Ask

The best negotiations always end in a win-win. Rather than fixating on dropping the sales price—something builders resist because it can affect future appraisals—think creatively about what would really give you the most value.

Sure, a price cut might save you a little on your monthly payment. But what if the builder covered all your closing costs? That could save you $10,000 to $20,000 in cash you need right now.

Expert Tip: Don't just ask for "more." Be specific. Frame your desired incentive as a solution to a problem. For instance, "The upfront cost of closing is a hurdle for us. If you could cover those fees, we'd be ready to sign the contract this week."

Try proposing a combination of perks. A builder might say no to a $20,000 price reduction, but they could very well say yes to $10,000 toward closing costs plus a $10,000 credit for the design center. This strategy protects their base price while still delivering a ton of value to you. Finally, once you agree on the terms, make sure every single detail is documented clearly in the purchase agreement.

Don't Get Blindsided: Common Pitfalls and Red Flags

Builder incentives can be a massive win, but it’s crucial to read the fine print. Some deals come with strings attached that can seriously water down the value. A classic move is to tie a fantastic incentive to a specific requirement, like using the builder's in-house or preferred lender.

The Preferred Lender Trap

So, the builder dangles a carrot: they'll cover $15,000 in closing costs, but you have to use their lending partner. The potential problem is that lender might have higher interest rates or fees than you'd find shopping around on your own. You might save cash upfront but pay more every month for the next 30 years.

To sidestep this, always get a loan estimate from at least one outside lender. Pit that offer against the builder's preferred lender and run the numbers. Sometimes, the builder's deal is genuinely the best one. Other times, you'll save more in the long run by securing your own financing.

Breaking Down the "Free Upgrade"

Another lure to watch out for is the "free upgrade" package. A builder might advertise a free gourmet kitchen, but you have to ask where that "free" money is really coming from. Often, the value of the package is inflated, or the base price of the home is already padded to cover the cost.

Your best defense here is good old-fashioned research. Look up the specific models of the appliances or the exact type of flooring they're offering. This gives you a clear picture of the true dollar value and helps you see if you're getting a genuine deal.

Crucial Advice: If I can give you one piece of advice, it's this: get every single incentive, promise, and detail in writing. Your purchase agreement must explicitly list every perk, credit, and concession. Verbal promises are worth nothing if they're not in the contract.

Vague Language and Handshake Deals

A sales rep might casually say they'll "take care of" the lot premium or "throw in" the blinds. Those words mean absolutely nothing until they are officially documented.

Make sure the contract language is crystal clear. It shouldn't just say "design center credit." It needs to be specific: "$10,000 credit to be used at the builder's design center for buyer-selected upgrades." This level of detail protects you and the builder, preventing any "he said, she said" arguments down the road as you build your dream North Texas home.

Putting It All Together: Real-World Scenarios in North Texas

Theory is one thing, but let's see how this all plays out in the real world. Every buyer's financial picture is different. What works for a young family building on acreage won't be the right fit for a retiree planning their dream home. It’s all about matching the incentive to your biggest need.

The Young Family Building on Acreage Near Weatherford

Picture a young couple with two kids who just snagged a few beautiful acres outside Weatherford. Their top priority is building a family home without wiping out their savings. For them, cash is king.

They’re looking at a $550,000 custom home and get two different offers.

Offer A: Straight Price Cut: The builder knocks $25,000 off the top, bringing the total home price down to $525,000.

Offer B: The Financial Relief Package: This one includes a $15,000 credit for closing costs and a 2-1 mortgage rate buydown (which costs the builder about $10,000).

For this family, Offer B is almost certainly the smarter move. The $15,000 in closing cost help means less cash they have to bring to the table right now. On top of that, the rate buydown lowers their mortgage payments significantly for the first two years. The instant gratification of a price cut is tempting, but the practical, immediate relief from Offer B solves their most pressing financial concerns.

The Retiree Couple in Granbury

Now, let's head over to Granbury. A retired couple has a healthy down payment for their $600,000 forever home. They aren't worried about upfront costs; their focus is on getting specific features for aging in place comfortably and safely.

The builder presents two options:

Offer A: Design Center Credit: A $20,000 allowance to spend on any upgrades they want.

Offer B: Accessibility & Efficiency Package: The builder offers to include a zero-entry shower, widen all interior doorways, and upgrade the HVAC to a high-efficiency model. The value of these items totals around $18,000.

In this case, Offer B is the hands-down winner. A design credit is nice, but Offer B directly gives them the functional upgrades they want for the long haul, plus the added bonus of lower utility bills. It’s tailored, practical, and ensures their home is ready for the future.

The Barndominium Builder on a Rural Glen Rose Property

Finally, let's look at someone building a barndominium on a rural lot near Glen Rose. They’ve fallen in love with a specific lot that has a great view—and a hefty lot premium.

For their $450,000 project, the builder offers two deals:

Offer A: The Lot Premium Waiver: The builder agrees to completely waive the $20,000 premium for their chosen lot.

Offer B: The Flex Cash Offer: The builder offers $15,000 in "flex cash" that can be used for closing costs, upgrades, or a price reduction.

Here, Offer A provides the most direct and powerful value. Getting that $20,000 lot premium wiped out is a pure, dollar-for-dollar saving on a fixed cost they can't otherwise avoid. While the flex cash is versatile, it simply doesn’t match the impact of eliminating that premium.

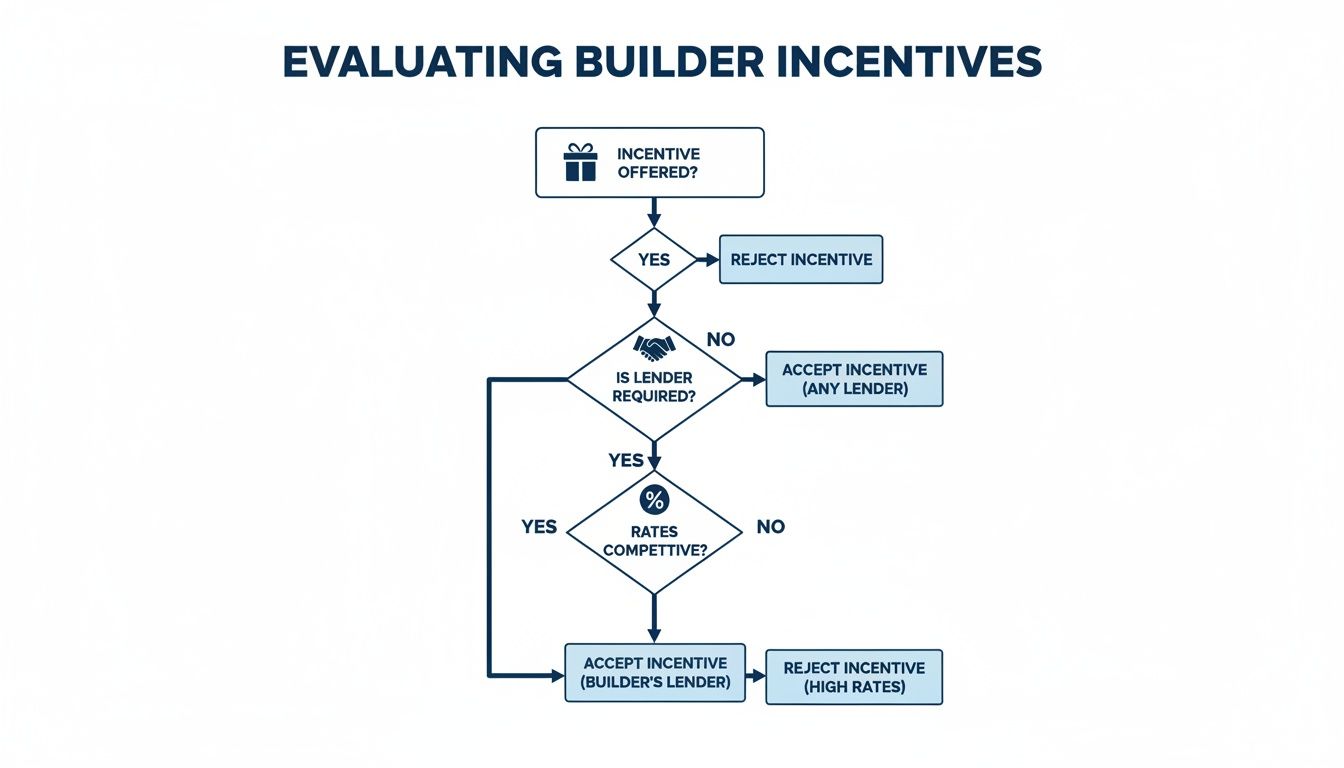

My Key Takeaway: The best incentive is the one that solves your biggest problem. It could be a lack of cash for closing, a need for specific features, or the high cost of a piece of land. Always connect the offer back to your personal goals.

This decision tree gives you a visual guide to working through these choices when a builder presents an incentive package.

As the flowchart shows, it’s critical to look at any lender requirements tied to an offer. Always compare the full picture to make sure you're getting a true net benefit.

Comparing Incentive Packages A vs. B

To make this even clearer, let's put two hypothetical offers side-by-side for a $500,000 custom home. This table breaks down how different incentives appeal to different buyer priorities.

Feature | Incentive Package A (Price-Focused) | Incentive Package B (Upgrade & Closing-Focused) | Which Buyer Is It For? |

|---|---|---|---|

Total Value | $25,000 | $25,000 | Both packages offer the same total value, but deliver it in very different ways. |

Price Reduction | $20,000 off the home price | $5,000 off the home price | Package A is better for buyers who want to lower their loan amount and build equity. |

Closing Cost Assistance | $5,000 toward closing | $10,000 toward closing | Package B is a huge win for cash-conscious buyers needing less out-of-pocket. |

Upgrade Allowance | None | $10,000 design center credit | Package B appeals to buyers who want high-end finishes but have a tight budget. |

Primary Benefit | Lower long-term loan amount | Immediate cash savings and personalized features | It’s a classic trade-off: long-term savings vs. short-term financial relief. |

Ultimately, deciding between these two packages comes down to your personal financial situation. Do you have plenty of cash on hand but want a lower monthly payment for the next 30 years? Package A is your best bet. Are you stretching to cover the down payment and have your heart set on that upgraded kitchen? Package B is the clear choice.

The Custom Builder Approach to Lasting Value

Working with a production builder often involves a song and dance around flashy, temporary promotions. But when you partner with a local, family-owned custom home builder here in North Texas, the entire conversation around new home builder incentives shifts. It’s less about chasing a short-term deal and more about creating permanent, lasting value in the home itself.

This isn't about a transaction; it's about building a trusted relationship. Our process is grounded in transparency from that very first meeting. We work with you to build value directly into your home's plan from day one, starting with a clear, realistic budget for your dream home in Granbury or Weatherford.

A Different Kind of Incentive

Forget the generic promotions like a free appliance package you might not even want. We focus on what actually enhances your project and your lifestyle. We believe the best incentive is a beautifully crafted home that perfectly suits your family, delivered on time and within budget.

So, what does that look like in practice?

Strategic Material Selection: We might advise allocating more of the budget toward a high-efficiency HVAC system. For families building on rural properties near Glen Rose, this delivers real savings on energy bills for decades—a far better return than a closing cost credit.

Prioritizing Lifestyle Features: Instead of a restrictive design credit, we can help you value-engineer certain areas. This might free up funds for that expansive covered patio or outdoor kitchen you've been dreaming of, features that truly elevate life in North Texas.

Thoughtful Design Integration: For retirees building in our community, the most valuable "incentive" isn't a discount. It’s our expertise in designing a home with smart accessibility features like wider hallways or a zero-entry shower, ensuring your home remains comfortable and safe for years to come.

This collaborative approach means every dollar gets invested where it matters most to you. We're not trying to move inventory; we're helping you create a home that will serve your family for generations.

The Real Value Proposition

At the end of the day, the ultimate incentive a custom builder offers is the quality, craftsmanship, and peace of mind you get. When you can call the owners directly and work with a dedicated crew, you receive responsive service and meticulous attention to detail that’s nearly impossible to find elsewhere.

We see ourselves as your partner and advocate throughout the entire build. Our job is to give you honest guidance, find smart ways to maximize your investment, and make sure the final home exceeds your every expectation. A well-built home that stands the test of time is truly the greatest financial benefit of all.

At Gemini Homes, we believe the best incentive is a partnership built on trust and a final product that reflects true quality. If you're ready to discuss your vision and explore how we can build genuine, lasting value into your new North Texas home, let's connect. Learn more about our custom home building process and get in touch with our team.

Comments